IATA’s October data for global air freight markets showing that air cargo demand continued to improve but at a slower pace than the previous month and remains below previous year levels.

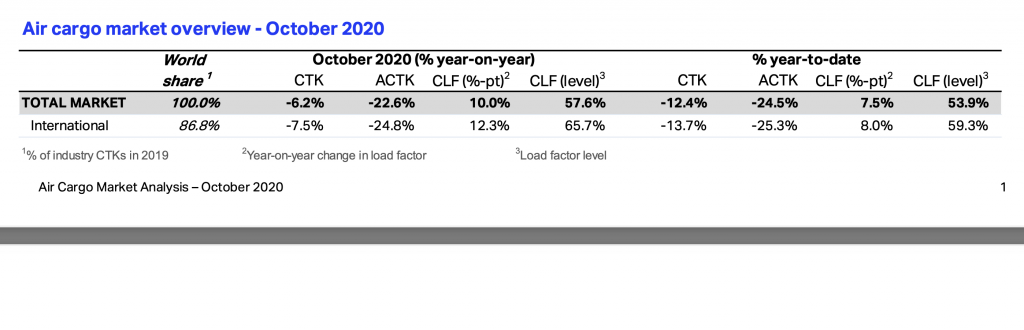

- Global demand, measured in cargo tonne-kilometers (CTKs*), was 6.2% below previous-year levels in October (-7.5% for international operations). That is an improvement from the 7.8% year-on-year drop recorded in September. However, the pace of recovery in October was slower than in September with month-on-month demand growing 4.1% (1.1% for international).

- Global capacity, measured in available cargo tonne-kilometers (ACTKs), shrank by 22.6% in October ( 24.8% for international operations) compared to the previous year. That is nearly four times larger than the contraction in demand, indicating the continuing and severe capacity crunch.

- Strong regional variations continue with North American and African carriers reporting year-on-year gains in demand (+6.2% and +2.2% respectively), while all other regions remained in negative territory compared to a year earlier.

- Improving performance is aligned with improvements in key economic indicators;

- The new export orders component of the manufacturing Purchasing Managers’ Index (PMI) stayed above the 50-mark for the second month in a row. Results above 50 indicate economic growth. This a significant development as the PMI had been in negative growth territory from mid-2018 through to August 2020;

- Global goods trade continued to trend upwards in recent months, according to the World Trade Organization. The uptick will not be sufficient to avoid a full-year decline of 9.2% compared to 2019. Much of this ground, however, will be regained in 2021 with an expectation of 7.2% annual growth;

- The Global Composite PMI which reflects changes in global output, employment, new business, backlogs and prices, indicates that economic recovery will continue in Q4/2020 despite a resurgence of the COVID-19 virus in many markets.

- The new export orders component of the manufacturing Purchasing Managers’ Index (PMI) stayed above the 50-mark for the second month in a row. Results above 50 indicate economic growth. This a significant development as the PMI had been in negative growth territory from mid-2018 through to August 2020;

“Demand for air cargo is coming back—a trend we see continuing into the fourth quarter. The biggest problem for air cargo is the lack of capacity as much of the passenger fleet remains grounded. The end of the year is always peak season for air cargo,” said Alexandre de Juniac, IATA’s Director General and CEO.

“That will likely be exaggerated with shoppers relying on e-commerce—80% of which is delivered by air. So the capacity crunch from the grounded aircraft will hit particularly hard in the closing months of 2020. And the situation will become even more critical as we search for capacity for the impending vaccine deliveries.”

October Regional Performance

- Asia-Pacific airlines saw demand for international air cargo fall 11.6% in October 2020 compared to the same month a year earlier. This was an improvement from the 14.6% fall in September 2020 and the second consecutive month of improvement. International capacity remained constrained in the region, down 28.7%. However, this was an improvement over the 31.8% fall in capacity the previous month. The region’s airlines reported the highest international load factor indicating a solid appetite for air cargo services.

- North American carriers posted a 1.3% increase in international demand in October compared to the previous year—the second month of growth in 10 months. This strong performance compared to the rest of the industry was driven by the Asia-North America routes, reflecting rising e-commerce demand for products manufactured in Asia and smaller capacity declines than other regions. The region’s domestic market decelerated slightly from September but remained robust. International capacity decreased by 16.6%.

- European carriers reported a decrease in demand of 11.9% in October compared to the previous year. This was an improvement from the 15.6% fall in September 2020. Air cargo in the region has been largely unaffected by the resurgence of the COVID-19 virus. International capacity decreased 28% an improvement from the 32.6% fall the previous month.

- Middle Eastern carriers reported a decline of 1.9% in year-on-year international cargo volumes in October, unchanged from September. However, the pace of recovery in October was slower than in September with month-on-month demand, improving 6.0% and 2.5% respectively. The weaker performance is driven by less demand in Africa-Middle East trade lanes. International capacity decreased by 22.7%.

- Latin American carriers reported a decline of 12.5% in international cargo volumes in October compared to the previous year. This was a significant improvement from the 22.2% fall in September 2020. The pace of month-on-month recovery was the strongest of all regions in October with demand climbing by 4%. The region’s improved year-on-year performance can be partly attributed to weak growth in the same period last year. However, improving operating conditions in a few key markets including Brazil and recovering cargo capacity also contributed. International capacity decreased 29.1% compared with up from 32.1% in September.

- African airlines saw demand increase by 2.8% year-on-year in October. This was lower than the 12.1% growth in September. Despite this the region still posted the strongest increase in international demand. The slight weakening in performance can be attributed to a slowdown in the Asia-Africa market where demand decelerated by 19 percentage points year-on-year. International capacity decreased by 20.8%.