AP Moller-Maersk improved profitability across the business during the third quarter 2020 and delivered strong free cash flow despite the negative impact on global economies from the COVID-19 pandemic.

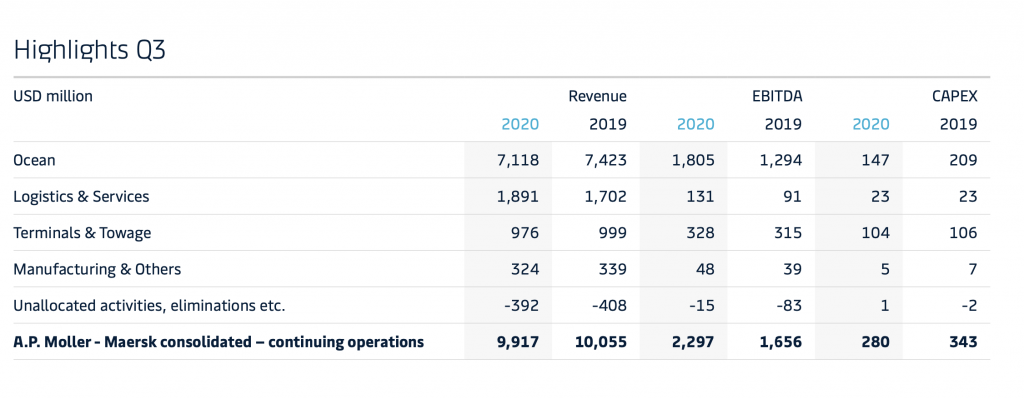

The Danish shipping and logistics giant grew earnings before interest, tax, depreciation and amortisation (EBITDA) 39% to $2.3bn with revenue decreasing 1.4% to $9.9bn.

The performance increase was based on a stringent costs control, agile capacity management, strong focus on customer offerings with further traction in uptake of digital services, and some benefit from a sequential demand recovery compared to the second quarter.

Said Søren Skou, CEO of AP Moller-Maersk: “Despite COVID-19 negatively affecting activities in most of our businesses, our disciplined execution of the strategy led to solid earnings and cash flow growth in Q3.

“At the same time, we managed to further integrate and simplify the organisation in Ocean & Logistics, we closed the acquisition of KGH Customs Services and continued the integration of Performance Team, supporting our strong financial performance in Logistics & Services.”

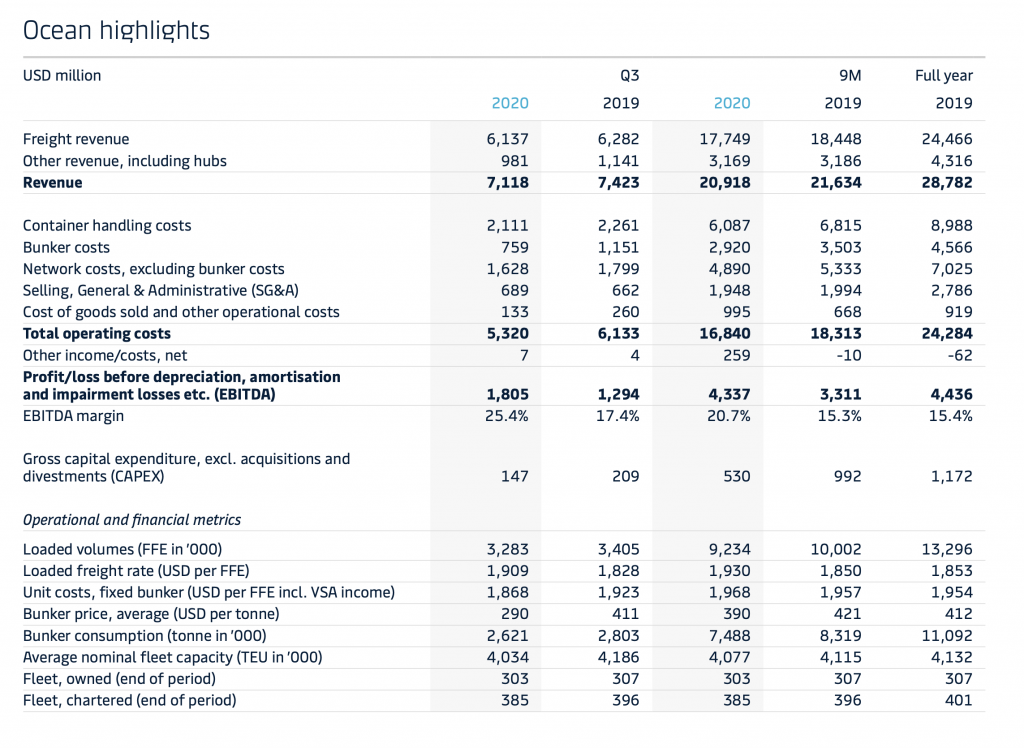

The main performance driver this quarter was Ocean which, despite decreasing volumes of 3.6% improved profitability by $511m to $1.8bn, reaching an EBITDA margin of 25.4% on the back of a continued agile capacity deployment, lower costs and a temporary spike in short-term freight rates due to a sudden demand pick-up on some routes.

Logistics & Services Revenue and gross Profit

The performance was strongly supported by Logistics & Services which benefitted from significant demand in supply chain management, intermodal and the acquired Performance Team.

In Q3, revenue in Logistics & Services grew 11% and profitability increased by 44%, achieving an EBITDA of $131m up from $91m in 2019, despite restructuring costs of $40m.

In Terminals & Towage, our effort to become a world-class operator enabled us to continue to expand margins and grow earnings, despite lower volumes and revenue.

Cash return on invested capital (CROIC), last twelve months, increased from 9.9% to 13.9% due to stronger cash flow from operating activities and lower gross CAPEX.

Return on invested capital (ROIC), last twelve months, increased from 3% to 5.9% as earnings improved and invested capital declined slightly.

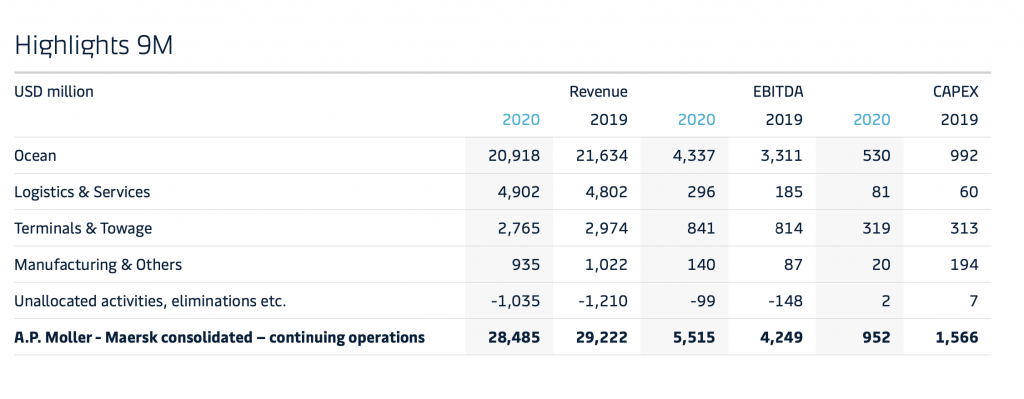

The free cash flow generation of $3bn in the first nine months of 2020, allowed the company to return cash to shareholders, finance acquisitions and reduce debt with net interest-bearing debt decreasing further to $10.8bn by the end of Q3 compared to $11.7bn by the end of 2019.

Søren Skou added: “Throughout the pandemic, our main priorities have been keeping our employees safe, keeping our global network and ports operating to serve our customers and supporting the societies we are part of. This continues to be our focus as demand has begun to partially recover.

“Our progress in earnings and in our transformation allows us to look confidently past the extraordinary 2020, however we remain well aware of the high level of uncertainty the pandemic and associated lock downs continue to pose in the coming quarters.”

Share buy-back programme

Given the strong performance and cash generation, the Board of Directors has decided to initiate a new share buy-back programme of DKK 10bn (approximately $1.6bn) over a period of up to 15 months, the first tranche of which ($500m) is expected to start in December. The remaining part of the share buy-back is subject to shareholder approval at the next Annual General Meeting in March 2021.

Guidance for 2020 and CAPEX

Given the current momentum across the business, AP Moller-Maersk expects, as announced on 17 November 2020, EBITDA before restructuring and integration costs in the range of $8bn to $8.5bn from previously between $7.5bn to $8bn as announced on 13 October 2020.

The global demand growth for containers is expected to contract by 4-5% in 2020 due to COVID-19.

Organic volume growth in Ocean is now expected to be slightly below the average market growth from previously in line with or slightly below the market.

For 2020, the guidance on capital expenditures (CAPEX) is expected to be $1.5bn, and with the expectation of a high cash conversion (cash flow from operations compared to EBITDA).

For 2021-2022, the accumulated guidance on capital expenditures is expected to be between $4.5bn and $5.5bn with the expectation of a high cash conversion.